By Dr. Taylor Christensen, Guest Writer

By Dr. Taylor Christensen, Guest Writer

I grew up believing in the conventional wisdom that the cheapest way to own a car is to “buy used and drive it until the wheels fall off.” But as I started digging into this topic a lot more in preparation for replacing both our cars (they went bad at the same time), I found that this isn’t strictly true. Let me explain.

Minimize the Annual Cost of Owning a Car

Just to be clear at the outset, my sole goal with this analysis was to find out how to minimize the annual cost of owning a car—I ignored convenience, luxury, safety features, and environmental impact. All I considered was the total cost per year. This is probably similar to how a frugal med student or resident would be approaching the task, but it’s also relevant to anyone interested in accelerating FIRE.

And for the rest of you—the people who are willing to pay more for luxury, newer safety features, environment, etc.—this analysis provides a means for quantifying exactly how much more you will be paying annually to have those extras, which I’ll demonstrate with concrete numbers at the end of this article.

Analyzing the Most Economical Way to Own a Car

All right, on to how I framed the analysis. Determining the cheapest way to own a car ultimately boils down to answering two different questions:

- What is the lowest-cost period of a car’s lifespan?

- Which model of car has the lowest costs during that period?

Tackling the first question, check out this graph that demonstrates the answer. It assumes driving about 15,000 miles per year, although significantly more or fewer miles per year will not affect the general conclusion. Also, it only lists the four major costs of owning a vehicle. Others, such as routine maintenance, are smaller costs. They stay relatively flat over time, so they were left out for the sake of simplicity. You can click on the graphic to make it bigger.

This graph doesn’t fit every car’s lifespan perfectly, but the U-shaped curve principle seems to hold true pretty consistently. As is common knowledge, a new car is expensive to own in the first year because it depreciates about 10% in the first minute of owning it (maybe we should call this “first-minute depreciation”), and you combine that with the usual depreciation for the rest of that first year of ownership. But the real question is: why, contrary to popular belief, does the total annual cost start to rise as the car gets older?

Two main factors combine to cause this.

The Cost of Car Deprecation and Repairs

First, depreciation stays pretty much constant for more years and more miles than people realize. I’ll show some data on that when I talk more about depreciation below. If the graph were carried out to 15 or 20 years, you would certainly see that depreciation cost per year decrease, but the cost of repairs would still be increasing to offset that. That's my next point.

Second, the average annual cost of repairs of a vehicle increases over time. I’m not talking about the one-in-a-100 car we always hear about from our parents, that old faithful Toyota that went over 500,000 miles without needing any major repairs. I’m talking about the average of all vehicles that are that same model and approximately the same age and miles. Your old faithful Toyota may do very well for many years in a row, but chances are, in spite of all the TLC you’re giving, it will regress to the mean sooner or later. Your total cost of ownership will rise with it. Buying or keeping an old car and hoping it will have fewer maintenance costs than average is like betting on a single stock and hoping it will outperform the rest. This is not a sound investment strategy in stocks or in cars.

One more point to drive home the costs associated with owning a car later on in its lifespan: Think about the total cost of ownership for the unlucky person who owns a car at the very end of its life (not shown on the graph). Not only were they probably dealing with fairly high repair costs, but then, when their car finally required a repair that cost more than the worth of the car, they had to junk it. So, they also took a serious hit in depreciation that year (because its value instantly dropped from maybe around $2,000 to $0). This is something we extra want to avoid. The owner would have done a lot better financially by selling that old faithful car and buying a relatively new used car instead. (Ahem, like I would have done had I known that driving a 2003 Chrysler Town & Country with over 200,000 miles on it could have a transmission go out at any moment.)

More information here:

How to Get Rich by Driving a $5,000 Car

Other Costs of Owning a Car to Consider

I know there are opportunity costs that temper these arguments, and that is something you will have to account for in your own situation. Will the opportunity cost of having $20,000 or more tied up in a relatively new car make it more expensive to own than an older $5,000 car? It depends on whether you will actually be investing that additional $15,000 and what your expected investment returns are.

There are also psychological factors to consider. If you own that relatively new car, will you feel the need to fix every little ding and to wash it every time it rains? If so, that would definitely increase the cost of owning a newer car.

I also haven’t mentioned how insurance will be cheaper for an older car, but that is a smaller factor and it may be partially offset by worse gas mileage as the car ages.

Regardless, the conclusions from the graph point to a clear answer to the first question: The cheapest period of a car’s lifespan is probably somewhere in the 2- to 8-year-old range (maybe even later if it’s a more reliable car or has been driven fewer miles than average).

More information here:

Driving an Old Car to Save Money. Drive a Beater . . . Get Rich.

Which Model of Car Is the Cheapest During Ownership?

Now, on to the second question: Which model of car is the cheapest during that period of ownership? Let’s look separately at each of the big cost drivers.

The first and most straightforward one is fuel. Gas or electric, it’s easy to look at fuel economy ratings from the EPA (and also check other sources, such as Consumer Reports, because sometimes the EPA’s ratings are inaccurate due to their dated lab-based testing methodology). Then, using your local gas and electricity prices, compute how much it would cost to drive your average annual miles. If we assume 15,000 miles per year, gas at $3.50 per gallon, and electricity at $0.15 per kWh . . .

20 mpg = $2,630/year

35 mpg = $1,500/year

50 mpg = $1,050/year

100 mpge = $760/year

120 mpge = $630/year

140 mpge = $540/year

Going from a typical SUV to an electric vehicle could save over $2,000 per year in fuel!

Next, insurance. A big part of your auto insurance cost is you—your age, credit score, driving record, etc. But there are many vehicle-specific factors that can impact your annual cost of insurance as well, including the value of the vehicle, how expensive it is to repair, the safety features, etc. Newer vehicles tend to be more expensive to insure due to their higher value, but that’s not always the case because availability of parts, safety features, and anti-theft features bring that cost down.

There’s a website I discovered during my research, caredge.com, which has been really helpful. It has a ton of data on all the big costs of owning a car, and that includes estimates of the relative cost of insurance for each specific model. This is a good place to get a quick estimate of the relative annual costs of insurance for the different models you’re looking at. For example, a Subaru Forester is estimated to cost $1,440 per year vs a Chevy Bolt at $1,830 per year.

And the last major cost component, which is usually the largest and definitely the most complex, is depreciation. Estimates are that depreciation accounts for an average of about 40% of the total cost of owning a vehicle. But people seem to think that once they own a car, depreciation doesn’t exist! This is probably because depreciation isn’t noticed (i.e., doesn’t affect your bank account) until the time comes to replace their vehicle and they find out how much they can sell it for. They aren’t feeling that loss in value every year like they would if one of their investments slowly decreased each time they logged into their account.

A common misunderstanding about depreciation is that you can always reduce it by buying a cheaper vehicle. The lower the purchase price, the less to depreciate, right? Sometimes this is true, but often it is not. The key is minimizing the difference between your upfront purchase price and your eventual resale price. For example, depreciation is less if you buy a $30,000 car and sell it five years later for $25,000 compared to buying a $10,000 car and selling it five years later for $4,000. The takeaway here is to focus less on the upfront purchase price and more on the predicted annual depreciation.

There are many written analyses online and many YouTube videos talking about how to predict and reduce depreciation, but they tend to oversimplify the topic by assuming depreciation is a single thing. In reality, there are several different subtypes of depreciation. I already mentioned “first-minute depreciation” above, but there are others. To illustrate, take a look at these graphs below. I’ll show the graphs first, and then I’ll discuss some conclusions I drew from them and others about the different types of depreciation.

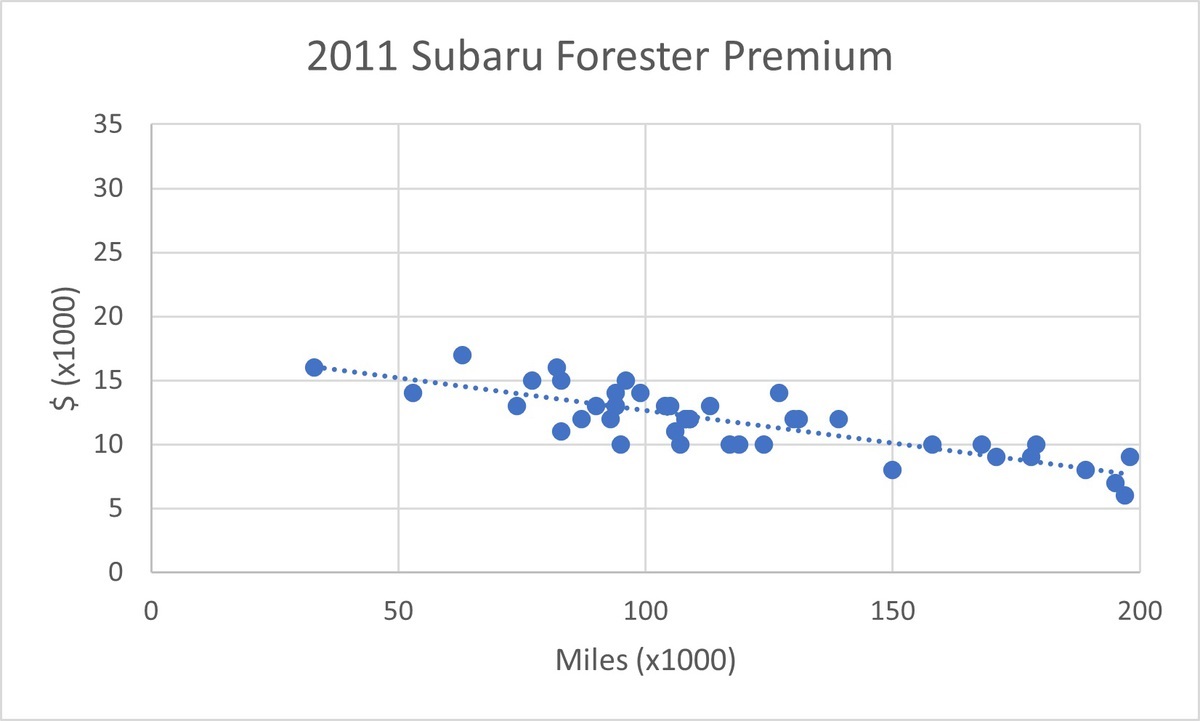

To make each graph, I searched all used vehicles of a specific make, model, year, and trim on cars.com and then plotted every single one of them according to its miles and price. You can click on the images below to make them bigger.

Yes, these took a little while to make. But my wife and I got really fast at reading and typing numbers. We chose to analyze Subaru Foresters because that was our car that got totaled in a wreck (right when the transmission went out in our “old faithful” van), so we were initially thinking of replacing the Forester with another one.

The overall trends are intuitive: older cars and cars with more miles on them are cheaper. But that simplistic assessment is not helpful when trying to calculate how much the car will cost you in depreciation. Instead, let’s take a closer look and make some more useful inferences. I’ve since done this analysis with several other cars, and the patterns are consistent. For any of you math types out there, I only had Excel add those linear trendlines (least squares) to each graph after they passed the eyeball test for linearity. There weren’t enough data points in the 0-20,000 miles range to confidently assess linearity for the first 20,000 miles, but my experience with the data suggests that the downward slope is a little bit larger in that range.

First, look at the slope of each line—it indicates the “miles depreciation” of the car. The flatter the slope, the less the car will depreciate with each mile you drive it. Numbers I’ve seen are typically around $0.05 -$0.10 per mile, but keep in mind, that’s from looking mostly at non-luxury five-seater cars. Since the line is surprisingly linear, that means if it costs you $0.05 per mile at 20,000 miles, it will still cost you about $0.05 per mile at 150,000 miles. This surprised me—I thought miles depreciation would decrease over the life of the car, but it isn’t true, even past 150,000 miles.

Now, compare different years of the same trim at 100,000 miles. With a little interpolation (because I didn’t graph every single year), you can see that each year the car ages, it loses about $1,000. That is what I call the “age depreciation,” and even going from 2012 to 2011 (and I verified this going from 2011 to 2010 as well) gives about that same amount of age depreciation. The car is over 10 years old by now and still, age depreciation remains linear! So, if you own a 2012 Subaru Forester and it’s just sitting in your garage never being driven, it is costing you about $1,000 per year of age depreciation. Of course, eventually age depreciation will slow down, but it really surprised me that it remains linear even past 10 years.

Did you notice that there is an exception to the $1,000 per year rule? Going from 2018 to 2016, you would expect the price to decrease by $2,000, but it actually depreciates by $3,000. This is what I call “generation depreciation.” The current generation of the Forester is from 2018-present. The last year of the prior generation was 2017, and, based on the numbers on cars.com (graph not shown), it averages about $2,000 cheaper than an equivalent 2018. Apparently, car shoppers don’t want a vehicle from the previous generation (I get it—their designs and features are dated), so they will apparently only be willing to buy one if it’s discounted by the equivalent of a whole extra year. You could avoid this generation depreciation if you buy a vehicle from the previous generation. But be careful—often the newer generation is more fuel-efficient and has more safety features, which means the newer generation will probably have lower fuel and insurance costs.

Now compare the higher-end Limited trim to the middle-of-the-range Premium trim. The Limited had an MSRP of about $3,000 more than the Premium, but it’s only worth about $1,000 more now. I guess used car buyers don’t highly value those premium features, such as leather and sunroofs and power liftgates, so a car can also have a “high-end trim depreciation.” I didn’t graph enough higher-end trims to know for sure, but I suspect that high-end trim depreciation is mostly completed after the first three or four years of the vehicle being on the road. That means, if you choose to buy a 4-year-old Subaru Forester Limited, you might pay an extra $1,000 upfront, but you can also probably re-sell it in five years for $1,000 more. I guess that’s nice if you want the extra features, but it does mean you will have to look at vehicles a little later into their lifespan.

In summary, here are all the types of depreciation I discovered:

- First-minute depreciation

- Age depreciation

- Miles depreciation

- Generation depreciation

- High-end trim depreciation

The big limitation to this data is that they are a snapshot, so I am drawing conclusions about changes to a car’s value over time based on looking at older cars of the same model. At least these general trends are consistent with what I’m seeing on caredge.com, where their aggregate depreciation calculations look similar but are based on longitudinal data. I wish they would de-aggregate their calculations into the different types of depreciation so I could compare more precisely.

The reason I think it’s important to mention the “snapshot” limitation to this data is because it means they do not take into account market trends over time, which can impact depreciation greatly. For example, I suspect that cars with poor fuel economy will start depreciating faster now that so many very-fuel-efficient cars (including electrics) have come out in the last few years. It’s something to keep in mind if you’re buying a less-fuel-efficient vehicle. And the pandemic-induced new-car shortage has raised prices for all used vehicles to the point where a new car’s first-minute depreciation is, in some cases, nonexistent, which means it’s probably worthwhile to at least get a quote on a new car to compare to the used prices you’re seeing.

Anyway, let’s put the magnitude of the different types of depreciation into perspective. The two biggest ones are age depreciation and miles depreciation. From what I’ve seen, age depreciation is probably about $1,000 per year for a typical non-luxury five-seater car. As I said before, typical miles depreciation seems to be $0.05-$0.10 per mile—which, assuming 15,000 miles per year, works out to $750-$1,500 per year. The generation depreciation will probably only hit you once during your ownership period, and if it’s $1,000, divide that one-time cost over seven years and it equals less than $150 per year. You can avoid the first-minute depreciation and high-end trim depreciation altogether by not getting a brand new car or a vehicle with high-end trim.

Whew. Depreciation is more complex, isn’t it?

Now that we’ve explored each of the major costs of ownership, let’s see how I used all that information to guide my efforts to answer the second question of discovering the lowest-cost models.

I first decided that fuel costs, age depreciation, and miles depreciation are the most important factors. If you drive more miles than average, fuel costs and miles depreciation are even more important in your analysis. I also decided to worry less about insurance costs because, even though it’s a large annual expense, it’s much less variable from model to model (within the non-luxury five-seater market, at least), so the difference will usually be no more than $300 per year.

Since depreciation figures are more difficult to come by, I started by narrowing down my options based on the EPA’s and Consumer Reports’ lists of the most fuel-efficient vehicles, and then I analyzed the depreciation of each of them after that.

I quickly found that electric vehicles tend to be more expensive from a depreciation standpoint. They are also less efficient than their stated mpge (miles per gallon equivalent) in cold weather. Those two factors, plus their limited range and spotty charging station availability where we typically drive when we go on trips, led me to take all electric vehicles off my shortlist. Maybe this will be different in 5-8 years when I do this analysis again.

This left me with a very manageable list of cars to analyze using a shortcut version of the scatterplot method above and corroborating that with the numbers on caredge.com. Then, it came down to regional availability of good deals on those cars.

There you have it. My answer to both questions.

Would you like to see the financial impact of all this effort?

Initially, because my wife loved her dearly departed Forester so much, we were planning on using the $13,000 that insurance gave us to buy another Forester that would cost around that much, thus avoiding spending any more money upfront. Then, we would plan to drive that car into the ground. We thought that was the frugal way to go about it. Here’s the first-year cost prediction of that decision using our own numbers (16,000 miles per year, $3.80 per gallon, personal insurance estimates):

- One-year total cost estimate: 2011 Subaru Forester

- Fuel (23 mpg): $2,640

- Aggregate depreciation: $2,120 ($1,000 per year age depreciation, $0.07 per mile miles depreciation)

- Insurance: $1,000

- Maintenance and repairs: $1,490

= Total: $7,250

Instead, we went with a 2020 Honda Insight. Again, costs are calculated using our own numbers, including an mpg adjustment for weather conditions since hybrids are less efficient in cold weather:

- One-year total cost estimate: 2020 Honda Insight

- Fuel (48 mpg): $1,160

- Aggregate depreciation: $1,800 ($1,000 per year age depreciation, $0.05 per mile miles depreciation)

- Insurance: $1,750

- Maintenance and repairs: $220

- Opportunity cost: $600 ($12,000 earning 5%)

= Total: $5,530

Let’s do a little analysis of those numbers.

First, even with the opportunity cost of having about $12,000 more tied up in a more expensive vehicle in that first year, we are still saving $1,720. Not bad!

Second, even though some of the savings is in decreased depreciation, a lot of it is in decreased fuel and repair costs, which means we will have more money in our pocket along the way. This more than cancels out any interest we would have earned by investing the extra $12,000, so the opportunity cost drag does not even really apply after the first year. Therefore, our savings will be more like $2,320 in year 2 (but probably more because the cost of repairs for the 2011 Subaru will increase much faster than the 2020 Honda).

Third, consider what those savings mean over time. If you’re a two-car family saving $4,000 per year by buying lower-cost-per-year vehicles, you could invest that $4,000 per year at 6% from age 25 until you retire at age 65 and have an extra $620,000. That’s a lot of cruises. All while driving newer, safer, lower-stress vehicles. (I certainly am excited about the prospect of no longer driving a van with a broken sliding door that is too heavy for my kids to open themselves and that doesn’t produce enough heat for me to stay warm in the winter without a blanket on my legs.)

For anyone who is less worried about saving money, this analysis empowers you to calculate how much more per year that luxury vehicle you’ve had your eye on would cost.

For example, maybe your dream car is a 2021 Tesla Model S Plaid. A very rough estimate of the total cost of ownership per year would be around $15,000 (primarily because depreciation would likely be a little more than $10,000 per year). Is the marginal benefit of a Tesla over a Honda Insight worth an extra $10,000 per year? Are there other uses for that $10,000 that you would enjoy more? These are the questions you have to answer for yourself, and now you can gather the data needed to formulate an informed answer.

Let’s do away with our parents’ wisdom of buying a used vehicle and driving it into the ground. Let’s also do away with the assumption that driving an old beater is the path to financial success. Instead, I recommend buying a relatively new vehicle that has low fuel costs and low depreciation and owning it for less than 10 years.

Do you think it's a good idea to buy an older car and drive it into the ground? Or should you get a newer car with more safety features that might depreciate faster? Should you finally purchase that Tesla? Comment below!

[Editor's Note: Taylor J. Christensen, MD, is an internal medicine physician and health policy researcher who has a passion for Excel spreadsheets and usually blogs at clearthinkingonhealthcare.com. This article was submitted and approved according to our Guest Post Policy. We have no financial relationship.]

The post The Cheapest Way to Own a Car appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.